Analytics as a Service is Largest and Fastest Growing Opportunity through 2023. Enterprise Data Syndication is Key Data as a Service Opportunity

Speak directly to the analyst to clarify any post sales queries you may have.

Telecommunications service providers acquire and maintain substantial structured and unstructured (Big) data. Leading carriers have centralized Subscriber Data Management (SDM) systems, which consolidate and organize data from various sources such as HLR, HSS, and other data repositories. In addition, carriers have access to a plethora of data from various "Big Data" sources such as OSS/BSS, system monitoring and performance management systems including Self Organizing Networks (SON).

Big Data and related Analytics solutions open a vast array of applications and opportunities for telecom carriers to offer services in multiple industry verticals. Solutions for managing unstructured data are evolving beyond systems aligned towards primarily human-generated data (such as social networking, messaging, and browsing habits) towards increasingly greater emphasis upon machine-generated data found across many industry verticals. For example, manufacturing and healthcare are anticipated to create massive amounts of data that may be rendered useful only through advanced analytics and various Artificial Intelligence (AI) technologies. Emerging networks and systems such as IoT and edge computing will generate substantial amounts of unstructured data, which will present both technical challenges and market opportunities for operating companies and their vendors.

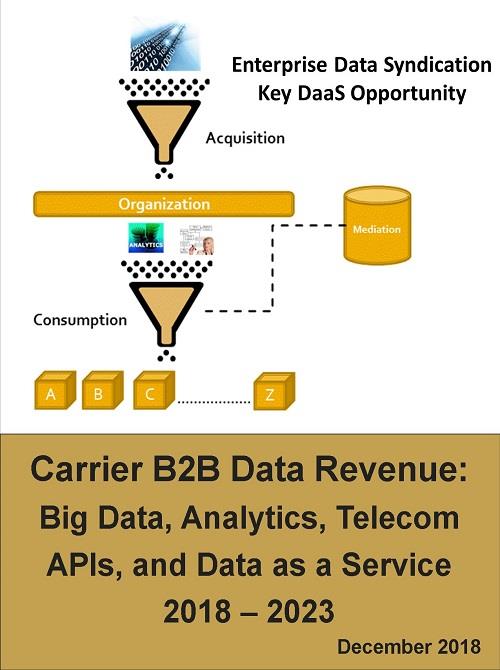

Network operators may sell data in a "Data as a Service" (DaaS) model to various market sectors including retail and hospitality, media, utilities, financial services, healthcare and pharmaceutical, telecommunications, government, homeland security, and the emerging industrial Internet vertical. DaaS is defined as any service offered wherein users can access vendor provided databases or host their own databases on vendor managed systems.

This research evaluates telecom data, analytics, APIs, and provides a quantitative and qualitative and assessment of carrier prospects for B2B revenue as a DaaS provider including forecast data and key insights respectively. It provides an in-depth assessment of the global Big Data market, including business case issues/analysis, application use cases, vendor landscape, value chain analysis, and a quantitative assessment of the industry with forecasting from 2018 to 2023. This research also evaluates the technologies, companies, strategies, and solutions for DaaS.

It assesses business opportunities for enterprise use of own data, others data, and a combination of both. It also analyzes opportunities for enterprise to monetize their own data through various third-party DaaS offerings. Additionally, it evaluates opportunities for DaaS in major industry verticals as well as the future outlook for emerging data monetization. Forecasts include global and regional projections by Sector, Data Collection, Source, and Structure from 2018 to 2023. This research is also the most comprehensive research covering the telecom API and programmable telecoms ecosystem including players, platforms, tools, solutions, and service offerings.

Select Findings:

- Total global Telecom API related revenue will reach $319.6B by 2023

- Telecom API support of IoT remains a high priority cellular operator-only opportunity

- North America and Western Europe represent the two largest regional markets for DaaS

- Edge Computing related Telecom API revenue will reach $395M in North America by 2023

- IoT DaaS is growing nearly three times as fast as non-IoT DaaS, with much of it streaming data

- Global IoT platform and authentication API revenue reaches $5.3B and $9.2B respectively by 2019

- Structured data market remains greater than unstructured, but the latter will overtake the former

- Machine-sourced data is growing twice as fast as non-machine data, largely due to IoT apps and services

Target Audience:

- IoT companies

- Network service providers

- Systems integration companies

- Big Data and Analytics companies

- Advertising and media companies

- Enterprise across all industry verticals

- Cloud and IoT product and service providers

Select Report Benefits:

- Identify key Big Data players and strategies

- Understand business case for enterprise Big Data

- DaaS segmentation by Structure, Source, Sector, and Collection

- Identify leading companies and solutions for Telecom API enabled apps and services

- Identify leading DaaS companies, strategies, and solutions offering enterprise solutions

- Understand the market dynamics, players, and outlook for communication enabled apps

- Understand the market dynamics for the Data as a Service market including leading services

With the purchase of this report at the Multi-user License or greater level, you will have access to one hour with an expert analyst who will help you link key findings in the report to the business issues you're addressing. This will need to be used within three months of purchase.

This report also includes a complimentary Excel file with data from the report for purchasers at the Site License or greater level.

Table of Contents

Data as a Service (DaaS) Market: Enterprise, Industrial, Public, and Government DaaS 2018 – 2023

1.0 Executive Summary

1.1 Global Data as a Service Market

1.2 Data as a Service Market by Data Type

1.3 Data as a Service Market by Region

2.0 Data as a Service Technologies

2.1 Cloud Computing and DaaS

2.2 Database Approaches and Solutions

2.2.1 Relational Database Management System

2.2.2 NoSQL

2.2.3 Hadoop

2.2.4 High Performance Computing Cluster

2.2.5 OpenStack

2.3 Data as a Service and the XaaS Ecosystem

2.4 Open Data Center Alliance

2.5 Market Sizing by Horizontal

3.0 Data as a Service Market

3.1 Market Overview

3.1.1 Understanding Data as a Service

3.1.2 Data Structure

3.1.3 Specialization

3.1.4 Vendors

3.2 Vendor Analysis and Prospects

3.2.1 Large Vendors

3.2.2 Mid-sized Vendors

3.2.3 Small Vendors

3.2.4 Market Sizing

3.3 Data as a Service Market Drivers and Constraints

3.3.1 Data as a Service Market Drivers

3.3.1.1 Business Intelligence and DaaS Integration

3.3.1.2 The Cloud Enabler DaaS

3.3.1.3 XaaS Drives DaaS

3.3.2 Data as a Service Market Constraints

3.3.2.1 Need for Data Integration

3.3.2.2 Issues Relating to Data-as-a-Service Integration

3.4 Barriers and Challenges to DaaS Adoption

3.4.1 Enterprises Reluctance to Change

3.4.2 Responsibility of Data Security Externalized

3.4.3 Security Concerns

3.4.4 Cyber Attacks

3.4.5 Unclear Agreements

3.4.6 Complexity is a Deterrent

3.4.7 Lack of Cloud Interoperability

3.4.8 Service Provider Resistance to Audits

3.4.9 Viability of Third-party Providers

3.4.10 No Move of Systems and Data is without Cost

3.4.11 Lack of Integration Features in the Public Cloud results in Reduced Functionality

3.5 Market Share and Geographic Influence

3.6 Vendors

4.0 Data as a Service Strategies

4.1 General Strategies

4.1.1 Tiered Data Focus

4.1.2 Value-based Pricing

4.1.3 Open Development Environment

4.2 Strategies for Emerging Market Opportunities

4.2.1 Communication Service Providers and DaaS

4.2.1.1 Service Ecosystem and Platforms

4.2.1.2 Bringing to Together Multiple Sources for Mash-ups

4.2.1.3 Developing Value-added Services as Proof Points

4.2.1.4 Open Access to all Entities including Competitors

4.2.2 Internet of Things and Data as a Service

4.2.2.1 Data as a Service is a Perfect Match for IoT

4.2.2.2 IoT Management for DaaS

4.2.2.3 Integrating IoT Data for DaaS

4.2.2.4 IoT Data as a Service requires Data Mediation

4.2.3 Edge Networks and Data as a Service

4.2.3.1 Mobile Edge Computing

4.2.3.2 Data from the Edge: MEC and Data as a Service

4.3 Service Provider Strategies

4.3.1 Telecom Network Operators

4.3.2 Data Center Providers

4.3.3 Managed Service Providers

4.4 Infrastructure Provider Strategies

4.4.1 Enable New Business Models

4.5 Application Developer Strategies

5.0 Data as a Service Applications

5.1 Business Intelligence

5.2 Development Environments

5.3 Verification and Authorization

5.4 Reporting and Analytics

5.5 Data as a Service in Healthcare

5.6 Data as a Service and Wearable Technology

5.7 Data as a Service in the Government Sector

5.8 Data as a Service for Media and Entertainment

5.9 Data as a Service for Telecoms

5.10 Data as a Service for Insurance

5.11 Data as a Service for Utilities and Energy Sector

5.12 Data as a Service for Pharmaceuticals

5.13 Data as a Service for Financial Services

6.0 Market Outlook and Future of Data as a Service

6.1 Security Concerns

6.2 Cloud Trends

6.2.1 Hybrid Computing

6.2.2 Multi-Cloud

6.2.3 Cloud Bursting

1.1 General Data Trends

6.3 Enterprise Leverages own Data and Telecom

6.3.1 Web APIs

6.3.2 SOA and Enterprise APIs

6.3.3 Cloud APIs

6.3.4 Telecom APIs

6.4 Data Federation Emerges for Data as a Service

7.0 Data as a Service Market Analysis and Forecasts 2018 – 2023

7.1 DaaS Market by Sector: Business, Public, and Government

7.1.1 DaaS Market for Public Data

7.1.2 DaaS Market for Business Data (Enterprise and Industrial)

7.1.3 DaaS Market for Government Data

7.2 DaaS Market by Source: Machine and Non-Machine Data

7.3 DaaS Market by Data Collection: IoT and Non-IoT Data

7.4 DaaS Markets by Hosting Type: Private, Public, and Hybrid

7.5 DaaS Markets by Pricing Model

7.6 DaaS Market by Service

7.7 DaaS Markets by Industry Vertical

8.0 Regional DaaS Market Analysis and Forecasts 2018 – 2023

8.1 North America Data as a Service Market

8.1.1 North America: DaaS Market by Sector (Business, Public, and Government)

8.1.2 North America: DaaS Market for Public Data

8.1.2.1 North America: DaaS Markets by Solution using Public Data

8.1.3 North America: DaaS Market for Business Data

8.1.3.1 DaaS Markets by Solution using Business Data

8.1.4 North America: DaaS Market by Data Source (Machine and Non-machine)

8.1.5 North America: DaaS Market by Data Collection Type

8.1.6 North America: DaaS Markets Hosting Type

8.1.7 North America: DaaS Markets by Pricing Model

8.1.8 North America: DaaS Market by Service

8.1.9 North America: DaaS Market by Industry Vertical

8.2 South America Data as a Service Market

8.2.1 South America: DaaS Market by Sector (Business, Public, and Government)

8.2.2 South America: DaaS Market for Public Data

8.2.2.1 South America: DaaS Market Solution using Public Data

8.2.3 South America: DaaS Market for Business Data

8.2.3.1 DaaS Market by Solution using Business Data

8.2.4 South America: DaaS Market by Data Source Type

8.2.5 South America: DaaS Market by Data Collection Type

8.2.6 South America: DaaS Market Hosting Type

8.2.7 South America: DaaS Market by Pricing Model

8.2.8 South America: DaaS Market by Service

8.2.9 South America: DaaS Market by Industry Vertical

8.3 Western Europe Data as a Service Market

8.3.1 Western Europe: DaaS Market by Sector (Business, Public, and Government)

8.3.2 Western Europe: DaaS Market for Public Data

8.3.2.1 Western Europe: DaaS Market by Solution using Public Data

8.3.3 Western Europe: DaaS Market for Business Data

8.3.3.1 DaaS Market by Solution using Business Data

8.3.4 Western Europe: DaaS Market by Data Source Type

8.3.5 Western Europe: DaaS Market by Data Collection Type

8.3.6 Western Europe: DaaS Market Hosting Type

8.3.7 Western Europe: DaaS Market by Pricing Model

8.3.8 Western Europe: DaaS Market by Service

8.3.9 Western Europe: DaaS Market by Industry Vertical

8.4 Central & Eastern European Data as a Service Market

8.4.1 Central & Eastern Europe: DaaS Market by Sector (Business, Public, and Government)

8.4.2 Central and Eastern Europe: DaaS Market for Public Data

8.4.2.1 Central and Eastern Europe: DaaS Market by Solution using Public Data

8.4.3 Central and Eastern Europe: DaaS Market for Business Data

8.4.3.1 DaaS Market by Solution using Business Data

8.4.4 Central and Eastern Europe: DaaS Market by Data Source Type

8.4.5 Central and Eastern Europe: DaaS Market by Data Collection Type

8.4.6 Central and Eastern Europe: DaaS Markets Hosting Type

8.4.7 Central and Eastern Europe: DaaS Markets by Pricing Model

8.4.8 Central and Eastern Europe: DaaS Markets by Service

8.4.9 Central and Eastern Europe: DaaS Markets by Industry Vertical

8.5 Asia Pacific Data as a Service Market

8.5.1 Asia Pacific: DaaS Market by Sector (Business, Public, and Government)

8.5.2 Asia Pacific: DaaS Market for Public Data

8.5.2.1 Asia Pacific: DaaS Market by Solution using Public Data

8.5.3 Asia Pacific: DaaS Market for Business Data

8.5.3.1 DaaS Market by Solution using Business Data

8.5.4 Asia Pacific: DaaS Market by Data Source Type

8.5.5 Asia Pacific: DaaS Market by Data Collection Type

8.5.6 Asia Pacific: DaaS Market by Hosting Type

8.5.7 Asia Pacific: DaaS Markets by Pricing Model

8.5.8 Asia Pacific: DaaS Markets by Service

8.5.9 Asia Pacific: DaaS Market by Industry Vertical

8.6 Middle East and Africa Data as a Service Market

8.6.1 Middle East and Africa: DaaS Market by Sector (Business, Public, and Government)

8.6.2 Middle East & Africa: DaaS Market for Public Data

8.6.2.1 Middle East & Africa: DaaS Market by Solution using Public Data

8.6.3 Middle East & Africa: DaaS Market for Business Data

8.6.3.1 DaaS Market by Solution using Business Data

8.6.4 Middle East & Africa: DaaS Market by Data Source Type

8.6.5 Middle East & Africa: DaaS Market by Data Collection Type

8.6.6 Middle East & Africa: DaaS Markets Hosting Type

8.6.7 Middle East & Africa: DaaS Markets by Pricing Model

8.6.8 Middle East & Africa: DaaS Markets by Service

8.6.9 Middle East & Africa: DaaS Markets by Industry Vertical

9.0 Conclusions and Recommendations

9.1.1 Data as a Service and IoT

9.1.2 Data as a Service and CSP Data

9.1.3 Data as a Service and Enterprise

10.0 Appendix

10.1 Structured vs. Unstructured Data

10.1.1 Structured Database Services in Telecom

10.1.2 Unstructured Database Services in Telecom and Enterprise

10.1.3 Emerging Hybrid (Structured/Unstructured) Database Services

10.2 Data Architecture and Functionality

10.2.1 Data Architecture

10.2.1.1 Data Models and Modelling

10.2.1.2 DaaS Architecture

10.2.2 Data Mart vs. Data Warehouse

10.2.3 Data Gateway

10.2.4 Data Mediation

10.3 Data Governance

10.3.1 Data Security

10.3.2 Data Quality

10.3.3 Data Integration

10.4 Master Data Management

10.4.1 Understanding MDM

10.4.1.1 Transactional vs. Non-transactional Data

10.4.1.2 Reference vs. Analytics Data

10.4.2 MDM and DaaS

10.4.2.1 Data Acquisition and Provisioning

10.4.2.2 Data Warehousing and Business Intelligence

10.4.2.3 Analytics and Virtualization

10.4.2.4 Data Governance

10.5 Data Mining

10.5.1 Data Capture

10.5.1.1 Event Detection

10.5.1.2 Capture Methods

10.5.2 Data Mining Tools

Figures

Figure 1: Global Market for Data as a Service 2018 – 2023

Figure 2: Data as a Service Market by Data Type 2018 – 2023

Figure 3: Data as a Service Market by Region 2018 – 2023

Figure 4: Cloud Computing Service Model

Figure 5: Data as a Service Vertical and Horizontal Markets

Figure 6: Data as a Service Revenue by Region 2018 to 2023

Figure 7: Data as a Service Types and Functions

Figure 8: Ecosystem and Platform Models

Figure 9: Data as a Service need for Data Mediation

Figure 10: DaaS Mediation Use Case: Smartgrid

Figure 11: Internet of Things and Data as a Service

Figure 12: Telecom API Value Chain for DaaS

Figure 13: DaaS Verification and Authorization

Figure 14: Data as a Service Foundation is SOA

Figure 15: Cloud Services rely upon DaaS and APIs

Figure 16: Federated Data vs. Non-Federated Models

Figure 17: Federated Data at Functional Level

Figure 18: Federated Data at City Level

Figure 19: Federated Data at Global Level

Figure 20: Federation Requires Mediation Data

Figure 21: Mediation Data Synchronization

Figure 22: DaaS Market by Sector (Business, Public, and Government) 2018 – 2023

Figure 23: DaaS Market by Public Data sourced Solution 2018 – 2023

Figure 24: DaaS Market by Public Data sourced Solution 2018 – 2023

Figure 25: DaaS Market for Business Data 2018 – 2023

Figure 26: DaaS Market by type of Solutions using Business Data 2018 – 2023

Figure 27: DaaS Market for Government Data 2018 – 2023

Figure 28: DaaS Market by Source (Machine vs. Non-machine Data) 2018 – 2023

Figure 29: DaaS Market by Data Collection (IoT vs. Non-IoT Data) 2018 – 2023

Figure 30: DaaS Market by Hosting Type (Private, Public, and Hybrid) 2018 – 2023

Figure 31: DaaS Market by Pricing Model 2018 – 2023

Figure 32: DaaS Market by Service Type 2018 – 2023

Figure 33: DaaS Market Industry Vertical 2018 – 2023

Figure 34: North America DaaS by Sector 2018 – 2023

Figure 35: North America DaaS Market by Public Data Type 2018 – 2023

Figure 36: North America DaaS Market by Solution using Public Data 2018 – 2023

Figure 37: North America DaaS Market by Enterprise and Industrial Data 2018 – 2023

Figure 38: North America DaaS Market by Business Data Solution 2018 – 2023

Figure 39: North America: DaaS Market by Data Source Type 2018 – 2023

Figure 40: North America DaaS Market by Data Collection Type 2018 – 2023

Figure 41: North America DaaS Market by Hosting Type 2018 – 2023

Figure 42: North America DaaS Market by Pricing Model 2018 – 2023

Figure 43: North America DaaS Market by Service 2018 – 2023

Figure 44: North America DaaS Market by Industry Vertical 2018 – 2023

Figure 45: South America DaaS Market by Sector 2018 – 2023

Figure 46: South America DaaS Market by Public Data Type 2018 – 2023

Figure 47: South America DaaS Market by Solution using Public Data 2018 – 2023

Figure 48: South America DaaS Market by Enterprise and Industrial Data 2018 – 2023

Figure 49: South America DaaS Market by Solution using Business Data 2018 – 2023

Figure 50: South America DaaS Market by Data Source Type 2018 – 2023

Figure 51: South America DaaS Market by Data Collection Type 2018 – 2023

Figure 52: South America DaaS Market by Hosting Type 2018 – 2023

Figure 53: South America DaaS Market by Pricing Model 2018 – 2023

Figure 54: South America DaaS Market by Service 2018 – 2023

Figure 55: South America DaaS Market by Industry Vertical 2018 – 2023

Figure 56: Western Europe DaaS Market by Sector 2018 – 2023

Figure 57: Western Europe DaaS Market by Public Data Type 2018 – 2023

Figure 58: Western Europe DaaS Market by Solution using Public Data 2018 – 2023

Figure 59: Western Europe DaaS Market by Enterprise and Industrial Data 2018 – 2023

Figure 60: Western Europe DaaS Market by Solution using Business Data 2018 – 2023

Figure 61: Western Europe DaaS Market by Data Source Type 2018 – 2023

Figure 62: Western Europe DaaS Market by Data Collection Type 2018 – 2023

Figure 63: Western Europe DaaS Market by Hosting Type 2018 – 2023

Figure 64: Western Europe: DaaS Market by Pricing Model 2018 – 2023

Figure 65: Western Europe DaaS Market by Services 2018 – 2023

Figure 66: Western Europe DaaS Market by Industry Vertical 2018 – 2023

Figure 67: Central & Eastern Europe DaaS Market by Sector 2018 – 2023

Figure 68: Central & Eastern Europe DaaS Market by Public Data Type 2018 – 2023

Figure 69: Central & Eastern Europe DaaS Market by Solution using Public Data 2018 – 2023

Figure 70: Central & Eastern Europe DaaS Market for Business Data 2018 – 2023

Figure 71: Central & Eastern Europe DaaS Market by Solution using Business Data 2018 – 2023

Figure 72: Central & Eastern Europe DaaS Market by Data Source Type 2018 – 2023

Figure 73: Central & Eastern Europe DaaS Market by Data Collection Type 2018 – 2023

Figure 74: Central & Eastern Europe DaaS Market by Hosting Type 2018 – 2023

Figure 75: Central & Eastern Europe DaaS Market by Pricing Model 2018 – 2023

Figure 76: Central & Eastern Europe DaaS Market Service 2018 – 2023

Figure 77: Central & Eastern Europe DaaS Market by Industry Vertical 2018 – 2023

Figure 78: Asia Pacific DaaS Market by Sector 2018 – 2023

Figure 79: Asia Pacific DaaS Market by Public Data Type 2018 – 2023

Figure 80: Asia Pacific DaaS Market by Solution using Public Data 2018 – 2023

Figure 81: Asia Pacific DaaS Market for Business Data 2018 – 2023

Figure 82: Asia Pacific DaaS Market by Solution using Business Data 2018 – 2023

Figure 83: Asia Pacific DaaS Market by Data Source Type 2018 – 2023

Figure 84: Asia Pacific DaaS Market by Data Collection Type 2018 – 2023

Figure 85: Asia Pacific DaaS Market by Hosting Type 2018 – 2023

Figure 86: Asia Pacific DaaS Market by Pricing Model 2018 – 2023

Figure 87: Asia Pacific DaaS Market by Service 2018 – 2023

Figure 88: Asia Pacific DaaS Market by Industry Vertical 2018 – 2023

Figure 89: Middle East & Africa DaaS Market by Sector 2018 – 2023

Figure 90: Middle East & Africa DaaS Market by Public Data Type 2018 – 2023

Figure 91: Middle East & Africa DaaS Market by Solution using Public Data 2018 – 2023

Figure 92: Middle East & Africa DaaS Market for Business Data 2018 – 2023

Figure 93: Middle East & Africa DaaS Market by Solution using Business Data 2018 – 2023

Figure 94: Middle East & Africa DaaS Market by Data Source Type 2018 – 2023

Figure 95: Middle East & Africa DaaS Market by Data Collection Type 2018 – 2023

Figure 96: Middle East & Africa DaaS Market by Hosting Type 2018 – 2023

Figure 97: Middle East & Africa DaaS Market by Pricing Model 2018 – 2023

Figure 98: Middle East & Africa DaaS Market by Service 2018 – 2023

Figure 99: Middle East & Africa DaaS Market Industry Vertical 2018 – 2023

Figure 100: Hybrid Data in Next Generation Applications

Figure 101: Traditional Data Architecture

Figure 102: Data Architecture Modeling

Figure 103: DaaS Data Architecture

Figure 104: Location Data Mediation

Figure 105: Data Mediation in IoT

Figure 106: Data Mediation for Smartgrids

Figure 107: Enterprise Data Types

Figure 108: Data Governance

Figure 109: Data Flow

Figure 110: Processing Streaming Data

Tables

Table 1: Global Market for DaaS 2018 – 2023

Table 2: DaaS Market Data Type 2018 – 2023

Table 3: DaaS Market by Region 2018 – 2023

Table 4: DaaS Market by Sector (Business, Public, and Government) 2018 – 2023

Table 5: DaaS Market for Public Data Type 2018 – 2023

Table 6: DaaS Market by Public Data sourced Solution 2018 – 2023

Table 7: DaaS Market for Business Data 2018 – 2023

Table 8: DaaS Market by Solution Type using Business Data 2018 – 2023

Table 9: DaaS Market by Source (Machine vs. Non-Machine Data) 2018 – 2023

Table 10: DaaS Market by Data Collection Type (IoT vs. Non-IoT) 2018 – 2023

Table 11: DaaS Market by Hosting Type2018 – 2023

Table 12: DaaS Market by Pricing Model 2018 – 2023

Table 13: DaaS Market by Service 2018 – 2023

Table 14: DaaS Market by Industry Vertical 2018 – 2023

Table 15: North America DaaS Market by Sector 2018 – 2023

Table 16: North America DaaS Market for Type of Public Data 2018 – 2023

Table 17: North America DaaS Market by Solution using Public Data 2018 – 2023

Table 18: North America DaaS Market by Enterprise and Industrial Data 2018 – 2023

Table 19: North America DaaS Market by Solution using Business Data 2018 – 2023

Table 20: North America DaaS Market by Data Source (Machine vs. Non-machine) 2018 – 2023

Table 21: North America DaaS Market by Data Collection Type 2018 – 2023

Table 22: North America DaaS Market by Hosting Type 2018 – 2023

Table 23: North America DaaS Market by Pricing Model 2018 – 2023

Table 24: North America DaaS Market by Service 2018 – 2023

Table 25: North America DaaS Market by type of Industry 2018 – 2023

Table 26: South America DaaS Market by Sector 2018 – 2023

Table 27: South America DaaS Market by Public Data Type 2018 – 2023

Table 28: South America DaaS Market by Solution using Public Data 2018 – 2023

Table 29: South America DaaS Market by Enterprise and Industrial Data 2018 – 2023

Table 30: South America DaaS Market by Solution using Business Data 2018 – 2023

Table 31: South America DaaS Market by Data Source Type 2018 – 2023

Table 32: South America DaaS Market by Data Collection Type 2018 – 2023

Table 33: South America DaaS Market Hosting Type 2018 – 2023

Table 34: South America DaaS Market by Pricing Model 2018 – 2023

Table 35: South America DaaS Market by Service 2018 – 2023

Table 36: South America DaaS Market by Industry Vertical 2018 – 2023

Table 37: Western Europe DaaS Market by Sector 2018 – 2023

Table 38: Western Europe DaaS Market by Public Data Type 2018 – 2023

Table 39: Western Europe DaaS Market by Solution using Public Data 2018 – 2023

Table 40: Western Europe: DaaS Market for Business Data 2018 – 2023

Table 41: Western Europe: DaaS Market by Solution using Business Data 2018 – 2023

Table 42: Western Europe DaaS Market by Data Source Type 2018 – 2023

Table 43: Western Europe DaaS Market by Data Collection Type 2018 – 2023

Table 44: Western Europe DaaS Market by Hosting Type 2018 – 2023

Table 45: Western Europe DaaS Market by Pricing Model 2018 – 2023

Table 46: Western Europe DaaS Market by Service 2018 – 2023

Table 47: Western Europe DaaS Market by Industry Vertical 2018 – 2023

Table 48: Central & Eastern Europe DaaS Market by Sector 2018 – 2023

Table 49: Central & Eastern Europe DaaS Market by Public Data Type 2018 – 2023

Table 50: Central & Eastern Europe DaaS Market by Solution using Public Data 2018 – 2023

Table 51: Central & Eastern Europe DaaS Market for Business Data 2018 – 2023

Table 52: Central & Eastern Europe DaaS Market by Solution using Business Data 2018 – 2023

Table 53: Central & Eastern Europe DaaS Market by Data Source Type 2018 – 2023

Table 54: Central & Eastern Europe DaaS Market by Data Collection Type 2018 – 2023

Table 55: Central & Eastern Europe DaaS Market by Hosting Type 2018 – 2023

Table 56: Central & Eastern Europe DaaS Market by Pricing Model 2018 – 2023

Table 57: Central & Eastern Europe DaaS Market by Service 2018 – 2023

Table 58: Central & Eastern Europe DaaS Market by Industry Vertical 2018 – 2023

Table 59: Asia Pacific DaaS Market by Sector 2018 – 2023

Table 60: Asia Pacific DaaS Market by Public Data Type 2018 – 2023

Table 61: Asia Pacific DaaS Market by Solution using Public Data 2018 – 2023

Table 62: Asia Pacific DaaS Market for Business Data 2018 – 2023

Table 63: Asia Pacific DaaS Market by Solution using Business Data 2018 – 2023

Table 64: Asia Pacific DaaS Market by Data Source Type 2018 – 2023

Table 65: Asia Pacific DaaS Market by Data Collection Type 2018 – 2023

Table 66: Asia Pacific DaaS Market by Hosting Type 2018 – 2023

Table 67: Asia Pacific DaaS Market by Pricing Model 2018 – 2023

Table 68: Asia Pacific DaaS Market by Service 2018 – 2023

Table 69: Asia Pacific DaaS Market by Industry Vertical 2018 – 2023

Table 70: Middle East & Africa DaaS Market by Sector 2018 – 2023

Table 71: Middle East & Africa DaaS Market by Public Data Type 2018 – 2023

Table 72: Middle East & Africa DaaS Market by Solution using Public Data 2018 – 2023

Table 73: Middle East & Africa DaaS Market for Business Data 2018 – 2023

Table 74: Middle East & Africa DaaS Market by Solution using Business Data 2018 – 2023

Table 75: Middle East & Africa DaaS Market by Data Source Type 2018 – 2023

Table 76: Middle East & Africa DaaS Market by Data Collection Type 2018 – 2023

Table 77: Middle East & Africa DaaS Market by Hosting Type 2018 – 2023

Table 78: Middle East & Africa DaaS Market by Pricing Model 2018 – 2023

Table 79: Middle East & Africa DaaS Market by Service 2018 – 2023

Table 80: Middle East & Africa DaaS Market by Industry Vertical 2018 – 2023

Big Data Market: Business Case, Market Analysis and Forecasts 2018 – 2023

1 Executive Summary

2 Introduction

2.1 Big Data Overview

2.1.1 Defining Big Data

2.1.2 Big Data Ecosystem

2.1.3 Key Characteristics of Big Data

2.2 Research Background

2.2.1 Scope

2.2.2 Coverage

2.2.3 Company Focus

3 Big Data Challenges and Opportunities

3.1 Securing Big Data Infrastructure

3.1.1 Big Data Infrastructure

3.1.2 Infrastructure Challenges

3.1.3 Big Data Infrastructure Opportunities

3.2 Unstructured Data and the Internet of Things

3.2.1 New Protocols, Platforms, Streaming and Parsing, Software and Analytical Tools

3.2.2 Big Data in IoT will require Lightweight Data Interchange Format

3.2.3 Big Data in IoT will use Lightweight Protocols

3.2.4 Big Data in IoT will need Protocol for Network Interoperability

3.2.5 Big Data in IoT Demands Data Processing on Appropriate Scale

4 Big Data Technology and Business Case

4.1 Big Data Technology

4.1.1 Hadoop

4.1.2 NoSQL

4.1.3 MPP Databases

4.1.4 Others and Emerging Technologies

4.2 Emerging Technologies,Tools, and Techniques

4.2.1 Streaming Analytics

4.2.2 Cloud Technology

4.2.3 Google Search

4.2.4 Customize Analytical Tools

4.2.5 Internet Keywords

4.2.6 Gamification

4.3 Big Data Roadmap

4.4 Market Drivers

4.4.1 Data Volume & Variety

4.4.2 Increasing Adoption of Big Data by Enterprises and Telecom

4.4.3 Maturation of Big Data Software

4.4.4 Continued Investments in Big Data by Web Giants

4.4.5 Business Drivers

4.5 Market Barriers

4.5.1 Privacy and Security: The ‘Big’ Barrier

4.5.2 Workforce Re-skilling and Organizational Resistance

4.5.3 Lack of Clear Big Data Strategies

4.5.4 Technical Challenges: Scalability & Maintenance

4.5.5 Big Data Development Expertise

5 Key Sectors for Big Data

5.1 Industrial Internet and Machine-to-Machine

5.1.1 Big Data in M2M

5.1.2 Vertical Opportunities

5.2 Retail and Hospitality

5.2.1 Improving Accuracy of Forecasts and Stock Management

5.2.2 Determining Buying Patterns

5.2.3 Hospitality Use Cases

5.2.4 Personalized Marketing

5.3 Media

5.3.1 Social Media

5.3.2 Social Gaming Analytics

5.3.3 Usage of Social Media Analytics by Other Verticals

5.3.4 Internet Keyword Search

5.4 Utilities

5.4.1 Analysis of Operational Data

5.4.2 Application Areas for the Future

5.5 Financial Services

5.5.1 Fraud Analysis, Mitigation & Risk Profiling

5.5.2 Merchant-Funded Reward Programs

5.5.3 Customer Segmentation

5.5.4 Customer Retention & Personalized Product Offering

5.5.5 Insurance Companies

5.6 Healthcare and Pharmaceutical

5.6.1 Drug Development

5.6.2 Medical Data Analytics

5.6.3 Case Study: Identifying Heartbeat Patterns

5.7 Telecommunications

5.7.1 Telco Analytics: Customer/Usage Profiling and Service Optimization

5.7.2 Big Data Analytic Tools

5.7.3 Speech Analytics

5.7.4 New Products and Services

5.8 Government and Homeland Security

5.8.1 Big Data Research

5.8.2 Statistical Analysis

5.8.3 Language Translation

5.8.4 Developing New Applications for the Public

5.8.5 Tracking Crime

5.8.6 Intelligence Gathering

5.8.7 Fraud Detection and Revenue Generation

5.9 Other Sectors

5.9.1 Aviation

5.9.2 Transportation and Logistics: Optimizing Fleet Usage

5.9.3 Real-Time Processing of Sports Statistics

5.9.4 Education

5.9.5 Manufacturing

6 The Big Data Value Chain

6.1 Fragmentation in the Big Data Value

6.2 Data Acquisitioning and Provisioning

6.3 Data Warehousing and Business Intelligence

6.4 Analytics and Visualization

6.5 Actioning and Business Process Management

6.6 Data Governance

7 Big Data Analytics

7.1 The Role and Importance of Big Data Analytics

7.2 Big Data Analytics Processes

7.3 Reactive vs. Proactive Analytics

7.4 Technology and Implementation Approaches

7.4.1 Grid Computing

7.4.2 In-Database processing

7.4.3 In-Memory Analytics

7.4.4 Data Mining

7.4.5 Predictive Analytics

7.4.6 Natural Language Processing

7.4.7 Text Analytics

7.4.8 Visual Analytics

7.4.9 Association Rule Learning

7.4.10 Classification Tree Analysis

7.4.11 Machine Learning

7.4.12 Neural Networks

7.4.13 Multilayer Perceptron (MLP)

7.4.14 Radial Basis Functions

7.4.15 Geospatial Predictive Modelling

7.4.16 Regression Analysis

7.4.17 Social Network Analysis

8 Standardization and Regulatory Initiatives

8.1 Cloud Standards Customer Council

8.2 National Institute of Standards and Technology

8.3 OASIS

8.4 Open Data Foundation

8.5 Open Data Center Alliance

8.6 Cloud Security Alliance

8.7 International Telecommunications Union

8.8 International Organization for Standardization

9 Global Markets and Forecasts for Big Data

9.1 Global Big Data Markets 2018 – 2023

9.2 Regional Markets for Big Data 2018 – 2023

9.3 Leading Countries in Big Data

9.3.1 United States

9.3.2 China

9.4 Big Data Revenue by Product Segment 2018 – 2023

9.4.1 Database Management Systems

9.4.2 Big Data Integration Tools

9.4.3 Application Infrastructure and Middleware

9.4.4 Business Intelligence Tools and Analytics Platforms

9.4.5 Big Data in Professional Services

10 Key Big Data Players

10.1 Vendor Assessment Matrix

10.2 1010Data (Advance Communication Corp.)

10.3 Accenture

10.4 Actian Corporation

10.5 Alteryx

10.6 Amazon

10.7 Anova Data

10.8 Apache Software Foundation

10.9 APTEAN (Formerly CDC Software)

10.10 Booz Allen Hamilton

10.11 Bosch Software Innovations: Bosch IoT Suite

10.12 Capgemini

10.13 Cisco Systems

10.14 Cloudera

10.15 CRAY Inc.

10.16 Computer Science Corporation (CSC)

10.17 DataDirect Network

10.18 Dell EMC

10.19 Deloitte

10.20 Facebook

10.21 Fujitsu

10.22 General Electric (GE)

10.23 GoodData Corporation

10.24 Google

10.25 Guavus

10.26 HP Enterprise

10.27 Hitachi Data Systems

10.28 Hortonworks

10.29 IBM

10.30 Informatica

10.31 Intel

10.32 Jasper (Cisco Jasper)

10.33 Juniper Networks

10.34 Longview

10.35 Marklogic

10.36 Microsoft

10.37 Microstrategy

10.38 MongoDB (Formerly 10Gen)

10.39 MU Sigma

10.40 Netapp

10.41 NTT Data

10.42 Open Text (Actuate Corporation)

10.43 Opera Solutions

10.44 Oracle

10.45 Pentaho (Hitachi)

10.46 Qlik Tech

10.47 Quantum

10.48 Rackspace

10.49 Revolution Analytics

10.50 Salesforce

10.51 SAP

10.52 SAS Institute

10.53 Sisense

10.54 Software AG/Terracotta

10.55 Splunk

10.56 Sqrrl

10.57 Supermicro

10.58 Tableau Software

10.59 Tata Consultancy Services

10.60 Teradata

10.61 Think Big Analytics

10.62 TIBCO

10.63 Verint Systems

10.64 VMware (Part of EMC)

10.65 Wipro

10.66 Workday (Platfora)

11 Appendix: Big Data Support of Streaming IoT Data

11.1 Big Data Technology Market Outlook for Streaming IoT Data

11.1.1 IoT Data Management is a Ubiquitous Opportunity across Enterprise

11.1.2 IoT Data becomes a Big Data Revenue Opportunity

11.1.3 Real-time Streaming IoT Data Analytics becoming a Substantial Business Opportunity

11.2 Global Streaming IoT Data Analytics Revenue

11.2.1 Overall Streaming Data Analytics Revenue for IoT

11.2.2 Global Streaming IoT Data Analytics Revenue by App, Software, and Services

11.2.3 Global Streaming IoT Data Analytics Revenue in Industry Verticals

11.3 Regional Streaming IoT Data Analytics Revenue

11.3.1 Revenue in Region

11.3.2 APAC Market Revenue

11.3.3 Europe Market Revenue

11.3.4 North America Market Revenue

11.3.5 Latin America Market Revenue

11.3.6 ME&A Market Revenue

11.4 Streaming IoT Data Analytics Revenue by Country

11.4.1 Revenue by APAC Countries

11.4.2 Revenue by Europe Countries

11.4.3 Revenue by North America Countries

11.4.4 Revenue by Latin America Countries

11.4.5 Revenue by ME&A Countries

Figures

Figure 1: Big Data Ecosystem

Figure 2: Key Characteristics of Big Data

Figure 3: Big Data Use Cases in Industry Verticals

Figure 4: Big Data Stack

Figure 5: Framework for Big Data in IoT

Figure 2: NoSQL vs Legacy DB Performance Comparisons

Figure 7: Roadmap Big Data Technologies 2018 - 2030

Figure 8: The Big Data Value Chain

Figure 9: Big Data Value Flow

Figure 10: Big Data Analytics

Figure 11: Global Big Data Markets 2018 – 2023

Figure 12: Regional Big Data Markets 2018 – 2023

Figure 13: Database Management Systems 2018 – 2023

Figure 14: Data Integration and Quality Tools 2018 – 2023

Figure 15: Application Infrastructure and Middleware 2018 – 2023

Figure 16: Business Intelligence Tools and Analytics Platforms 2018 – 2023

Figure 17: Big Data in Professional Services 2018 – 2023

Figure 18: Big Data Vendor Ranking Matrix

Figure 19: Streaming IoT Data Sources Compared

Figure 20: Overall Streaming IoT Data Analytics

Tables

Table 1: Global Big Data Markets 2018 – 2023

Table 2: Regional Big Data Markets 2018 – 2023

Table 3: Big Data Markets by Product Segments 2018 – 2023

Table 4: Database Management Systems 2018 – 2023

Table 5: Data Integration Tools 2018 – 2023

Table 6: Application Infrastructure and Middleware 2018 – 2023

Table 7: Business Intelligence Tools and Analytics Platforms 2018 – 2023

Table 8: Big Data in Professional Services 2018 – 2023

Table 9: Big Data Analytics Platforms by Company

Table 10: Global Streaming IoT Data Analytics Revenue by App, Software, and Service

Table 11: Global Streaming IoT Data Analytics Revenue in Industry Vertical

Table 12: Retail Streaming IoT Data Analytics Revenue by Retail Segment

Table 13: Retail Streaming IoT Data Analytics Revenue by App, Software, and Services

Table 14: Telecom & IT Streaming IoT Data Analytics Rev by Segment

Table 15: Telecom & IT Streaming IoT Data Analytics Rev by App, Software, and Services

Table 16: Energy & Utilities Streaming IoT Data Analytics Rev by Segment

Table 17: Energy & Utilities Streaming IoT Data Analytics Rev by App, Software, and Services

Table 18: Government Streaming IoT Data Analytics Revenue by Segment

Table 19: Government Streaming IoT Data Analytics Revenue by App, Software, and Services

Table 20: Healthcare & Life Science Streaming IoT Data Analytics Revenue by Segment

Table 21: Healthcare & Life Science Streaming IoT Data Analytics Revenue by App, Software, and Services

Table 22: Manufacturing Streaming IoT Data Analytics Revenue by Segment

Table 23: Manufacturing Streaming IoT Data Analytics Revenue by App, Software, and Services

Table 24: Transportation & Logistics Streaming IoT Data Analytics Revenue by Segment

Table 25: Transportation & Logistics Streaming IoT Data Analytics Revenue by App, Software, and Services

Table 26: Banking and Finance Streaming IoT Data Analytics Revenue by Segment

Table 27: Banking & Finance Streaming IoT Data Analytics Revenue by App, Software, and Services

Table 28: Smart Cities Streaming IoT Data Analytics Revenue by Segment

Table 29: Smart Cities Streaming IoT Data Analytics Revenue by App, Software, and Services

Table 30: Automotive Streaming IoT Data Analytics Revenue by Segment

Table 31: Automotive Streaming IoT Data Analytics Revenue by Apps, Software, and Services

Table 32: Education Streaming IoT Data Analytics Revenue by Segment

Table 33: Education Streaming IoT Data Analytics Revenue by App, Software, and Services

Table 34: Outsourcing Service Streaming IoT Data Analytics Revenue by Segment

Table 35: Outsourcing Service Streaming IoT Data Analytics Revenue by App, Software, and Services

Table 36: Streaming IoT Data Analytics Revenue by Leading Vendor Platforms

Table 37: Streaming IoT Data Analytics Revenue in Region

Table 38: APAC Streaming IoT Data Analytics Revenue by Solution and Services

Table 39: APAC Streaming IoT Data Analytics Revenue in Industry Vertical

Table 40: APAC Streaming IoT Data Analytics Revenue by Leading Vendor Platforms

Table 41: Europe Streaming IoT Data Analytics Revenue by Solution and Services

Table 42: Europe Streaming IoT Data Analytics Revenue in Industry Vertical

Table 43: Europe Streaming IoT Data Analytics Revenue by Leading Vendor Platforms

Table 44: North America Streaming IoT Data Analytics Revenue by Solution and Services

Table 45: North America Streaming IoT Data Analytics Revenue in Industry Vertical

Table 46: North America Streaming IoT Data Analytics Revenue by Leading Vendor Platforms

Table 47: Latin America Streaming IoT Data Analytics Revenue by Solution and Services

Table 48: Latin America Streaming IoT Data Analytics Revenue in Industry Vertical

Table 49: Latin America Streaming IoT Data Analytics Revenue by Leading Vendor Platforms

Table 50: ME&A Streaming IoT Data Analytics Revenue by Solution and Services

Table 51: ME&A Streaming IoT Data Analytics Revenue in Industry Vertical

Table 52: ME&A Streaming IoT Data Analytics Revenue by Leading Vendor Platforms

Table 53: Streaming IoT Data Analytics Revenue by APAC Countries

Table 54: Japan Streaming IoT Data Analytics Revenue by Solution and Services

Table 55: Japan Streaming IoT Data Analytics Revenue in Industry Vertical

Table 56: China Streaming IoT Data Analytics Revenue by Solution and Services

Table 57: China Streaming IoT Data Analytics Revenue in Industry Vertical

Table 58: India Streaming IoT Data Analytics Revenue by Solution and Services

Table 59: India Streaming IoT Data Analytics Revenue in Industry Vertical

Table 60: Australia Streaming IoT Data Analytics Revenue by Solution and Services

Table 61: Australia Streaming IoT Data Analytics Revenue in Industry Vertical

Table 62: Streaming IoT Data Analytics Revenue by Europe Countries

Table 63: Germany Streaming IoT Data Analytics Revenue by Solution and Services

Table 64: Germany Streaming IoT Data Analytics Revenue in Industry Vertical

Table 65: UK Streaming IoT Data Analytics Revenue by Solution and Services

Table 66: UK Streaming IoT Data Analytics Revenue in Industry Vertical

Table 67: France Streaming IoT Data Analytics Revenue by Solution and Services

Table 68: France Streaming IoT Data Analytics Revenue in Industry Vertical

Table 69: Streaming IoT Data Analytics Revenue by North America Countries

Table 70: US Streaming IoT Data Analytics Revenue by Solution and Services

Table 71: US Streaming IoT Data Analytics Revenue in Industry Vertical

Table 72: Canada Streaming IoT Data Analytics Revenue by Solution and Services

Table 73: Canada Streaming IoT Data Analytics Revenue in Industry Vertical

Table 74: Streaming IoT Data Analytics Revenue by Latin America Countries

Table 75: Brazil Streaming IoT Data Analytics Revenue by Solution and Services

Table 76: Brazil Streaming IoT Data Analytics Revenue in Industry Vertical

Table 77: Mexico Streaming IoT Data Analytics Revenue by Solution and Services

Table 78: Mexico Streaming IoT Data Analytics Revenue in Industry Vertical

Table 79: Streaming IoT Data Analytics Revenue by ME&A Countries

Table 80: South Africa Streaming IoT Data Analytics Revenue by Solution and Services

Table 81: South Africa Streaming IoT Data Analytics Revenue in Industry Vertical

Table 82: UAE Streaming IoT Data Analytics Revenue by Solution and Services

Table 83: UAE Streaming IoT Data Analytics Revenue in Industry Vertical

Telecom API Market Outlook and Forecasts 2018 – 2023

1 Executive Summary

2 Introduction

2.1 About the Report

2.1.1 Topics Covered

2.1.2 Key Findings

2.1.3 Target Audience

2.2 Programmable Telecom

2.2.1 Programmable Telecom Definition

2.2.2 Programmable Telecom Purpose

2.2.3 Telecom Programmability Tools

2.2.3.1 Application Programming Interfaces (API)

2.2.3.2 Cloud Hosted Services

2.2.3.3 Communications Platform as a Service (CPaaS)

2.2.3.4 Graphical User Interfaces (GUI)

2.2.3.5 Open Source Telecom Software

2.2.3.6 Software Development Kits (SDK)

2.3 State of the Industry

3 Telecom API Overview

3.1 Role and Importance of Telecom APIs

3.2 Business Drivers for CSPs to Leverage APIs

3.2.1 Need for New Revenue Sources

3.2.2 Need for Collaboration with Development Community

3.2.3 B2B Services and Asymmetric Business Models

3.2.4 Emerging Need for IoT Mediation

3.3 Telecom API Categories

3.3.1 Access Management

3.3.2 Advertising and Marketing

3.3.3 Billing of Non-Digital Goods

3.3.4 Content Delivery

3.3.5 Directory and Registry Management

3.3.6 Enterprise Collaboration

3.3.7 IVR/Voice Solutions

3.3.8 Location Determination

3.3.9 M2M and Internet of Things

3.3.10 Messaging and other Non-Voice Communications

3.3.10.1 Text Messaging

3.3.10.2 Multimedia Messaging

3.3.11 Number Management

3.3.12 Payments including Purchaser Present Verification

3.3.13 Presence Detection

3.3.14 Real-time Communications and WebRTC

3.3.15 Subscriber Identity Management

3.3.16 Subscriber Profile Management

3.3.17 Quality of Service Management

3.3.18 Unified Communications and UCaaS

3.3.19 Unstructured Supplementary Service Data

3.3.20 Unwanted Call Management and Robo Calls

3.3.21 Voice/Speech

3.4 Telecom API Business Models

3.4.1 Three Business Model Types

3.4.1.1 Model One

3.4.1.2 Model Two

3.4.1.3 Model Three

3.4.2 The Asymmetric Business Model

3.4.3 Exposing APIs to Developers

3.4.4 Web Mash-ups

3.5 Segmentation

3.5.1 Users by Segment

3.5.2 Workforce Management

3.6 Competitive Issues

3.6.1 Reduced Total Cost of Ownership

3.6.2 Open APIs

3.6.3 Configurability and Customization

3.7 Applications that use APIs

3.8 Telecom API Revenue Potential

3.8.1 Standalone API Revenue vs. API enabled Revenue

3.8.2 Telecom API-enabled Mobile VAS Applications

3.8.3 Carrier Focus on Telecom API’s for the Enterprise

3.9 Telecom API Usage by Industry Segment

3.10 Telecom API Value Chain

3.10.1 Telecom API Value Chain

3.10.2 How the Value Chain Evolves

3.10.3 API Transaction Value Split among Players

3.11 API Transaction Cost by Type

3.12 Volume of API Transactions

4 API Aggregation

4.1 Role of API Aggregators

4.2 Total Cost of Operation with API Aggregators

4.2.1 Start-up Costs

4.2.2 Transaction Costs

4.2.3 Ongoing Maintenance/Support

4.2.4 Professional Services by Intermediaries

4.3 Aggregator API Usage by Category

4.3.1 API Aggregator Example: LocationSmart

4.3.2 Aggregation: Intersection of Two Big Needs

4.3.3 The Case for Other API Categories

4.3.4 Moving Towards New Business Models

5 Telecom API Marketplace

5.1 Data as a Service (DaaS)

5.1.1 Carrier Structured and Unstructured Data

5.1.2 Carrier Data Management in DaaS

5.1.3 Data Federation in the DaaS Ecosystem

5.2 API Marketplace Companies

5.2.1 Mashape

5.2.2 Mulesoft

5.2.3 TeleStax

5.3 Telecom API Ecosystem Vendors

5.3.1 APIs part of Infrastructure and Services Portfolio

5.3.1.1 Ericsson

5.3.1.2 Huawei

5.3.1.3 Nokia Networks

5.3.1.1 Ribbon Communications

5.3.2 API Capabilities Acquired via M&A

5.3.2.1 Amdocs

5.3.2.2 Aspect Software

5.3.2.3 BICS

5.3.2.4 CA Technologies

5.3.2.5 Cisco

5.3.2.6 Google

5.3.2.7 Oracle

5.3.2.8 Persistent Systems

5.3.2.9 Vonage

5.3.3 API Capabilities Independently Developed

5.3.3.1 Apidaze

5.3.3.2 Apifonica

5.3.3.3 Bandwidth Inc.

5.3.3.4 CLX Communications

5.3.3.5 Fortumo

5.3.3.6 hSenid Mobile

5.3.3.7 Hubtel

5.3.3.8 MessageBird

5.3.3.9 Syniverse

5.3.3.10 Telnyx

5.3.3.11 Tyntec

5.3.3.12 Twilio

5.3.3.13 Vidyo

5.4 Telecom Application Development

5.4.1 Communications-enabled App Marketplace

5.4.1.1 Market Opportunities and Challenges

5.4.1.2 Marketplace Facilitators

5.4.2 Improving Existing Apps and Services Marketplace

6 Telecom API Enabled App Use Cases

6.1 Monetization of Communications-enabled Apps

6.1.1 Direct API Revenue

6.1.2 Data Monetization

6.1.3 Cost Savings

6.1.4 Higher Usage

6.1.5 Churn Reduction

6.2 Use Case Issues

6.2.1 Security

6.2.2 Data Privacy

6.2.3 Interoperability

7 Communication Service Provider Telecom API Strategies

7.1 Carrier Market Strategy and Positioning

7.1.1 API Investment Stabilization

7.1.2 Carriers, APIs, and OTT

7.1.3 Leveraging Subscriber Data and APIs

7.1.4 Telecom API Standards

7.1.5 Telecom APIs and Enterprise

7.2 Select Network Operator API Programs

7.2.1 AT&T

7.2.2 Verizon Wireless

7.2.3 Vodafone

7.2.4 France Telecom (Orange)

7.2.5 Telefonica

7.3 Carrier Focus on Internal Telecom API Usage

7.3.1 The Case for Internal Usage

7.3.2 Internal Telecom API Use Cases

7.4 Carriers and OTT Service Providers

7.4.1 Allowing OTT Providers to Manage Applications

7.4.2 Carriers Lack the Innovative Skills to Capitalize on APIs Alone

7.5 Carriers and Value-added Services

7.5.1 Role and Importance of VAS

7.5.2 The Case for Carrier Communication-enabled VAS

7.5.3 Challenges and Opportunities for Carriers in VAS

8 API Enabled Application Developer Strategies

8.1 Treating Telecom APIs as a Critical Developer Asset

8.2 Judicious Choice of API Releases

8.3 Working alongside Carrier Programs

8.4 Developer Preferences: OTT Service Providers vs Carriers

9 Telecom API Vendor Strategies

9.1 General Strategies

9.1.1 Value Chain Enhancers and Development Facilitators

9.1.2 Moving from Platforms to Cloud-based CPaaS

9.2 Specific Strategies

9.2.1 Reliance upon SIP Trunking

9.2.2 Improving Existing Solutions

9.2.3 Increased Focus on Enterprise Solutions

9.2.4 Embracing Next Generation Use Cases

10 Telecom API Market Analysis and Forecasts

10.1 Global Telecom API Market 2018 – 2023

10.1.1 Total Telecom API Market

10.1.2 Telecom API Market by Category

10.1.3 Telecom API Market by Service Type

10.1.4 Telecom API Market by User Type

10.1.5 Telecom API Market by Network Technology

10.1.6 Telecom API Market by Deployment

10.1.7 Telecom API Market by Module

10.1.8 Telecom API Market by Stakeholder

10.2 Regional Telecom API Market 2018 – 2023

10.2.1 Telecom API Market by Region 2018 - 2023

10.2.2 North America Telecom API Market by API Category and Service Type 2018 - 2023

10.2.3 Europe Telecom API Market by API Category and Service Type 2018 – 2023

10.2.4 APAC Telecom API Market by API Category and Service Type 2018 – 2023

10.2.5 Middle East and Africa Telecom API Market by API Category and Service Type 2018 – 2023

10.2.6 Latin America Telecom API Market by API Category and Service Type 2018 – 2023

10.2.7 Top Ten Telecom API Markets 2018 – 2023

11 Technology and Market Drivers for API Market Growth

11.1 Service Oriented Architecture

11.2 Software Defined Networks

11.3 Virtualization

11.3.1 Network Function Virtualization

11.3.2 Virtualization beyond Network Functions

11.4 Internet of Things

11.4.1 IoT Definition

11.4.2 IoT Technologies

11.4.3 IoT Applications

11.4.4 IoT Solutions

11.4.5 IoT, DaaS, and APIs

11.5 IoT WANs and Telecom APIs

11.5.1 Cellular IoT WAN

11.5.2 Non-Cellular IoT WAN

11.5.1 Cellular vs. Non-Cellular IoT WAN Telecom API Needs

11.5.2 Telecom APIs for IoT Authentication and Platforms

12 Conclusions and Recommendation

12.1 Overall Telecom API Outlook

13 Appendix

13.1 Telecom API Definitions

13.2 More on Telecom APIs and DaaS

13.2.1 Tiered Data Focus

13.2.2 Value-based Pricing

13.2.3 Open Development Environment

13.2.4 Specific Strategies

13.2.4.1 Service Ecosystem and Platforms

13.2.4.2 Bringing to Together Multiple Sources for Mash-ups

13.2.4.3 Developing Value-added Services as Proof Points

13.2.4.4 Open Access to all Entities including Competitors

13.2.4.5 Prepare for Big Opportunities with the Internet of Things (IoT)

13.3 Monetizing IoT APIs

13.3.1 IoT API Business Models

13.3.2 Peer Support of Platforms, Devices, and Gateways

13.3.3 Supporting the API Developer Community

13.3.4 Data and Database Transactions

Figures

Figure 1: Communication Service Provider Assets

Figure 2: Next Generation CSP Assets driving Telecom API Usage

Figure 3: RCS and Telecom API Integration

Figure 4: Enterprise Dashboard

Figure 5: Enterprise Dashboard App Example

Figure 6: Telecom API Value Chain

Figure 7: API Transaction Value by Type

Figure 8: Volume of API Transactions for a Tier 1 Carrier 2018 - 2023

Figure 9: Cloud Services and APIs

Figure 10: Programmable Telecom Vendor Services Comparative Segmentation

Figure 11: GSMA OneAPI: Benefits to Stakeholders

Figure 12: AT&T Wireless API Catalog

Figure 13: Verizon Wireless API Program

Figure 14: France Telecom (Orange) API Program

Figure 15: Telefonica API Program

Figure 16: Carrier Internal Use of Telecom APIs

Figure 17: Global Telecom API Market 2018 – 2023

Figure 18: Global Telecom API Market Yearly Growth 2018 – 2023

Figure 19: Top Ten Telecom API Market Share by Country 2018 – 2023

Figure 20: Services Oriented Architecture

Figure 21: Global Connected IoT Things and Objects 2018 – 2023

Figure 22: IoT and Future Telecom API Topology

Figure 23: 3GPP IoT Proposals for LTE, Narrowband and 5G Network

Figure 24: LoRaWAN Network Architecture

Figure 25: Cellular vs. Non-Cellular IoT WAN Comparison

Figure 26: Different Data Types and Functions in DaaS

Figure 27: Ecosystem and Platform Model

Figure 28: Telecom API and Internet of Things Mediation

Figure 29: DaaS and IoT Mediation

Tables

Table 1: Global Telecom API Market by Category 2018 – 2023

Table 2: Global Telecom API Market Share by Category 2018 – 2023

Table 3: Global Telecom API Market by Service Type 2018 – 2023

Table 4: Global Telecom API Market Share by Service Type 2018 – 2023

Table 5: Global Telecom API Market by User Type 2018 – 2023

Table 6: Global Telecom API Market Share by User Type 2018 – 2023

Table 7: Global Telecom API Market by Network Technology 2018 – 2023

Table 8: Global Telecom API Market Share by Network Technology 2018 – 2023

Table 9: Global Telecom API Market by Deployment 2018 – 2023

Table 10: Global Telecom API Market Share by Deployment 2018 – 2023

Table 11: Global Telecom API Market by Module 2018 – 2023

Table 12: Global Telecom API Market Share by Module 2018 – 2023

Table 13: Global Telecom API Market by Stakeholder 2018 – 2023

Table 14: Global Telecom API Market Share by Stakeholder 2018 – 2023

Table 15: Telecom API Market by Region 2018 – 2023

Table 16: Telecom API Market Share by Region 2018 – 2023

Table 17: North America Telecom API Market by Category 2018 – 2023

Table 18: North America Telecom API Market by Service Type 2018 – 2023

Table 19: North America Telecom API Market by User Type 2018 – 2023

Table 20: North America Telecom API Market by Network Technology 2018 – 2023

Table 21: North America Telecom API Market by Deployment 2018 – 2023

Table 22: North America Telecom API Market by Module 2018 – 2023

Table 23: North America Telecom API Market by Stakeholder 2018 – 2023

Table 24: North America Telecom API Market by Country 2018 – 2023

Table 25: North America Telecom API Market Share by Country 2018 – 2023

Table 26: Europe Telecom API Market by Category 2018 – 2023

Table 27: Europe Telecom API Market by Service Type 2018 – 2023

Table 28: Europe Telecom API Market by User Type 2018 – 2023

Table 29: Europe Telecom API Market by Network Technology 2018 – 2023

Table 30: Europe Telecom API Market by Deployment 2018 – 2023

Table 31: Europe Telecom API Market by Module 2018 – 2023

Table 32: Europe Telecom API Market by Stakeholder 2018 – 2023

Table 33: Europe Telecom API Market by Country 2018 – 2023

Table 34: Europe Telecom API Market Share by Country 2018 – 2023

Table 35: APAC Telecom API Market by Category 2018 – 2023

Table 36: APAC Telecom API Market by Service Type 2018 – 2023

Table 37: APAC Telecom API Market by User Type 2018 – 2023

Table 38: APAC Telecom API Market by Network Technology 2018 – 2023

Table 39: APAC Telecom API Market by Deployment 2018 – 2023

Table 40: APAC Telecom API Market by Module 2018 – 2023

Table 41: APAC Telecom API Market by Stakeholder 2018 – 2023

Table 42: APAC Telecom API Market by Country 2018 – 2023

Table 43: APAC Telecom API Market Share by Country 2018 – 2023

Table 44: MEA Telecom API Market by Category 2018 – 2023

Table 45: MEA Telecom API Market by Service Type 2018 – 2023

Table 46: MEA Telecom API Market by User Type 2018 – 2023

Table 47: MEA Telecom API Market by Network Technology 2018 – 2023

Table 48: MEA Telecom API Market by Deployment 2018 – 2023

Table 49: MEA Telecom API Market by Module 2018 – 2023

Table 50: MEA Telecom API Market by Stakeholder 2018 – 2023

Table 51: MEA Telecom API Market by Country 2018 – 2023

Table 52: MEA Telecom API Market Share by Country 2018 – 2023

Table 53: Latin America Telecom API Market by Category 2018 – 2023

Table 54: Latin America Telecom API Market by Service Type 2018 – 2023

Table 55: Latin America Telecom API Market by User Type 2018 – 2023

Table 56: Latin America Telecom API Market by Network Technology 2018 – 2023

Table 57: Latin America Telecom API Market by Deployment 2018 – 2023

Table 58: Latin America Telecom API Market by Module 2018 – 2023

Table 59: Latin America Telecom API Market by Stakeholder 2018 – 2023

Table 60: Latin America Telecom API Market by Country 2018 – 2023

Table 61: Latin America Telecom API Market Share by Country 2018 – 2023

Table 62: Top Ten Telecom API Market by Country 2018 – 2023

Table 63: Global Connected Device by Non-IoT Product 2018 – 2023

Table 64: Global Connected Device by Consumer IoT Product 2018 – 2023

Table 65: Global Connected Device by Enterprise IoT Product 2018 – 2023

Table 66: Global Connected Device by Industrial IoT Product 2018 – 2023

Table 67: Global Connected Device by Government IoT Product 2018 – 2023

Companies Mentioned

- 1010data

- 3i Data Scraping

- Accenture PLC

- Actifio

- Acxiom Corporation

- Alibaba Group Holding Limited (China)

- Alteryx Ltd.

- Amazon Web Services, Inc. (AWS)

- Amdocs

- Apaleo Marketplace

- Apidaze

- Apifonica

- Appier.com

- Aspect Software

- AtScale Inc.

- Bandwidth

- BICS

- Bloomberg Finance L.P.

- CA Technologies

- Cisco Systems Inc.

- Clickfox

- CLX Communications

- Column technologies

- comScore Inc.

- Continental vAnalytics

- Coriolis Technologies

- Corporate360

- Crunchbase, Inc.

- CTERA

- Datameer

- Datasift Inc.

- DataStax Inc

- Dawex Systems

- DC Frontiers Pte. Ltd.

- Dell EMC

- Demandbase (Whotoo)

- Denodo Technologies

- Dow Jones & Company, Inc.

- Dremio

- EMC Corporation

- Equifax, Inc.

- Ericsson

- ESRI, Inc.

- Experian plc

- Facebook, Inc.

- Factiva

- Fico

- FirstRain, Inc.

- Fortumo

- GE Predix

- getsix group

- Gigaspaces

- Google Inc.

- Guavus Inc.

- Hewlett Packard Enterprise

- HG Data Company

- Hitachi Data Systems

- Hoover's

- Hortonworks

- hSenid Mobile

- Huawei

- Hubtel

- IBM Corporation

- IHS Inc

- Infochimps

- Infogix, Inc.,

- Informatica Corporation

- Information Builders Inc.

- Information Resources, Inc

- Infosys

- Intel

- Intercontinental Exchange, Inc.,

- Intuit

- Iota Foundation

- Ipedo

- IQM Corporation

- K2View

- KBC global

- LexisNexis Group

- LinkedIn Corporation

- LocationSmart

- MapR Technologies Inc

- MariaDB

- Mashape

- MasterCard Advisors

- MessageBird

- Microsoft Corporation

- Mighty AI, Inc.

- Mindtree

- Mobilewalla

- Moody's Corporation

- Morningstar, Inc

- Mulesoft

- Nielsen Holdings Plc

- Nokia Networks

- Opera Solutions LLC

- Optum, Inc.,

- Oracle Corporation

- Pentaho

- Persistent Systems

- PlaceIQ, Inc.

- Protel I/O

- Qlik Technologies Inc.

- Qubole

- Quest Software

- Rackspace

- Red Hat

- Ribbon Communications

- Salesforce.com

- SAP SE

- SAS Institute

- SiteMinder Exchange

- SlamData,

- SMARTe Inc.

- SnapLogic

- Snapshot (On Demand)

- Snowflake Computing

- Splunk

- Syniverse

- Talend

- TeleStax

- Telnyx

- Teradata

- Terbine

- Terracotta

- The Dun & Bradstreet Corporation

- The Weather Company, LLC

- Thomson Reuters Corp.

- ThoughtSpot Inc.

- TIBCO Software Inc

- Tresata

- Twilio

- Twitter, Inc.

- Tyntec

- Urban Mapping

- Verizon Communications, Inc.,

- Vidyo

- Vonage

- Wisers Information Limited

- Wolters Kluwer N.V

- workday

- Xignite

- ZertoZerto